Consider the pros and con's of a HELOC before you apply. HELOCs do not have closing costs. However, the interest you pay on funds that are used for personal expenses is not tax-deductible. You may end up spending too much on your HELOC and tap out equity. This can lead to high principal and interest costs. The good news? Interest rates are lower than traditional fixed-rate 30-year home equity loans.

Interest charges on funds from a HELOC used to pay off personal expenses are no longer tax deductible

You may wonder if HELOC interest payments are still tax deductible. The good news is that you still can up to $750,000 in interest payments on a HELOC. However, you won't be able to deduct the interest on funds used for personal expenses, such as home renovations. This is because the new tax law has changed the way that you can deduct interest payments for personal expenses.

Homeowners could previously deduct interest up to $100,000 from their HELOC. The new tax law limits the deduction to home improvements that increase your home's value. However, the improvements must be substantial in order to increase the home's overall market value. A substantial improvement is an improvement that significantly increases the value of the home, such as a new kitchen or extension.

The tax code stipulates that interest on a home equity credit line must be used to purchase collateral property. This does not include personal expenses.

HELOCs are available without closing costs

While a HELOC offers no closing cost, it is important for you to take into consideration all costs before making your final decision. Closing costs may be charged by the lender in addition to the interest rate. Before making a decision, you should shop around for lower costs. The typical closing costs range from 2% to 5 percent of the total credit line.

HELOCs are a form of revolving credit that utilizes the equity in your house as collateral. You can use the funds for many purposes, including home improvement and medical expenses. Lenders set the credit limit based on the equity in the home, and the "draw period" is typically ten years. After that, borrowers will need to start repaying the loan. If borrowers wish, they may be able renew the loan.

Some HELOC lenders charge closing costs, but these fees are usually minimal compared to other costs. The lender may charge an application fee, origination fee or notary fee as well as a title search fee. The lender will charge these fees to ensure that the loan is legal binding and not subject to any liens. You may also be charged by the lender for a credit check or an appraisal.

Higher interest rates than a 30-year fixed home equity loan

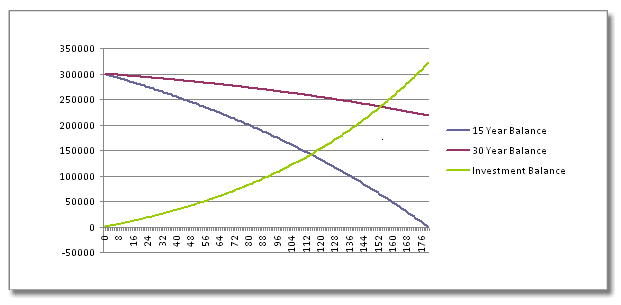

A home equity loan is a loan secured against the home's equity. The loan is paid in lump-sums and then interest-free over a predetermined period. A home equity credit line (HELOC) works in the same way as a credit card except that you only pay interest for the amount borrowed and not the total balance.

A home equity loan has a fixed-rate rate and a repayment period between 5 and 30 years. This means you will have the same interest rate regardless how the economy does. A fixed-rate home equity loan usually has lower interest rates than most other loans, with some even as low at 3%.

Home equity lines allow borrowers to borrow funds whenever they are needed. They can be used to finance a home renovation project or debt repayment. Home equity lines of credit have lower interest rates than other loans, but you will need a high credit score and a low debt-to-income ratio to qualify.

FAQ

What are the benefits of a fixed-rate mortgage?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. You won't need to worry about rising interest rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

Is it better buy or rent?

Renting is usually cheaper than buying a house. However, renting is usually cheaper than purchasing a home. The benefits of buying a house are not only obvious but also numerous. For instance, you will have more control over your living situation.

How many times may I refinance my home mortgage?

It depends on whether you're refinancing with another lender, or using a broker to help you find a mortgage. In both cases, you can usually refinance every five years.

How do you calculate your interest rate?

Interest rates change daily based on market conditions. The average interest rate for the past week was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

Can I get a second loan?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What are the three most important factors when buying a house?

The three most important things when buying any kind of home are size, price, or location. The location refers to the place you would like to live. Price refers how much you're willing or able to pay to purchase the property. Size refers to the space that you need.

How much money can I get to buy my house?

It depends on many factors such as the condition of the home and how long it has been on the marketplace. Zillow.com shows that the average home sells for $203,000 in the US. This

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to find houses to rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. It can be difficult to find the right home. When choosing a house, there are many factors that will influence your decision making process. These factors include price, location, size, number, amenities, and so forth.

To make sure you get the best possible deal, we recommend that you start looking for properties early. Ask your family and friends for recommendations. You'll be able to select from many options.