Saving money on interest is possible by getting a mortgage that uses a point system. This article discusses the costs and advantages of buying points. We'll also talk about when to buy points. We'll also discuss the tax benefits as well as the break-even point. Homeowners will love to make points investments on their mortgage.

Tax benefits

A 1-point mortgage is a mortgage expense, which can be deducted by some taxpayers. This mortgage expense has no tax benefits beyond the first $750,000 in loan total value. Points are paid upfront. They are not included in any other closing costs such title insurance, credit check fees or recording fees. The IRS allows points to be deducted as mortgage interest. This reduces taxable income, resulting in a lower tax bill and a higher refund. Before a mortgage point can being deducted, however, there are several conditions.

If you want to receive the most tax benefits from mortgage-points, you need to carefully consider how long your plan to remain in the home. For example, paying a point is a good idea if you plan to live in the home for at least seven years. However, if you are planning to sell or refinance your home soon, it might be wiser not to pay a mortgage points.

Cost

A mortgage point can lower your mortgage interest rate. They are great for homeowners who plan to live in their home for the long-term. They are not for everyone. A mortgage point program should only be considered if you plan on staying in your home long-term. It is important to consider your budget before making any final decisions.

Calculate how much you'll save over time before buying mortgage points. Your job situation and the size of your home will impact how much money you save each year. It is also important to calculate the breakeven period for your mortgage points.

Break-even point

In order to determine whether or not paying one mortgage point is worth it, calculate your break even point. Your financial situation, housing plans, and other factors will influence the calculation. Instead of paying points, consider buying lower mortgage rates to help you pay off your loan faster. Consider how long you intend to be living in your home. Paying a point if you are planning to move within the next ten years is not a great investment.

In addition to paying off the mortgage sooner, you can also refinance the mortgage at a lower interest rate. This will lower the monthly payments and will save money over time. Refinance a mortgage can be done in 36 months.

Points for buying

Points on a mortgage could help you lower your interest rate. However, this option might not be right for everyone. You should consider purchasing points only if you intend to stay in your home for a long time. Points purchase can lower your monthly loan payment and save you thousands in interest over the term of your loan.

Mortgage points are a special payment made at the closing of a mortgage that can lower your monthly payments and interest rate. This is also called "buying down your rate". Purchasing points will lower your mortgage payment in the long run, and get you closer to owning your own home sooner.

Deduction of tax

One point can be deducted from your mortgage loan amount when you're approved. These mortgage point can be listed on the settlement statement or Box 6 in Form 1098. They can also be deducted from the loan's life if you are approved under certain conditions. These criteria include whether the points were paid out of your own money or from the seller.

If you are claiming a deduction to pay a mortgage point, it is important that you only use the money for the purchase of a primary residence. You can't claim this deduction if your primary residence is rented.

FAQ

How do I calculate my rate of interest?

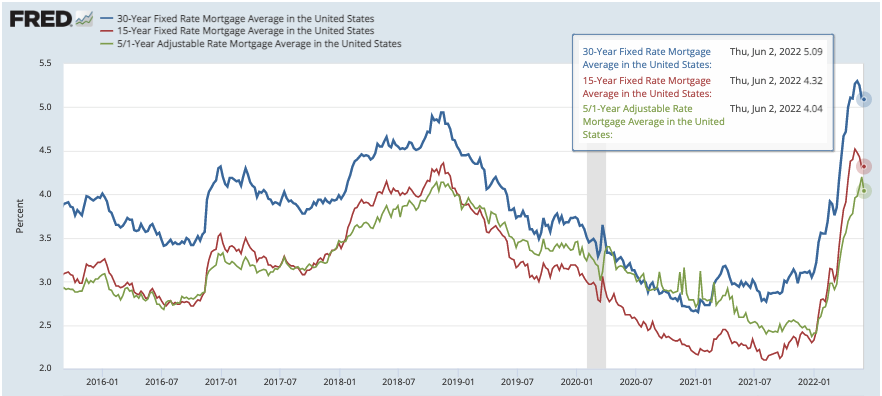

Market conditions impact the rates of interest. The average interest rate over the past week was 4.39%. Add the number of years that you plan to finance to get your interest rates. For example, if you finance $200,000 over 20 years at 5% per year, your interest rate is 0.05 x 20 1%, which equals ten basis points.

How much money should I save before buying a house?

It all depends on how many years you plan to remain there. Start saving now if your goal is to remain there for at least five more years. But if you are planning to move after just two years, then you don't have to worry too much about it.

Do I need flood insurance?

Flood Insurance protects you from flooding damage. Flood insurance protects your possessions and your mortgage payments. Learn more about flood insurance here.

Can I get a second loan?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is used to consolidate or fund home improvements.

How much will my home cost?

It all depends on several factors, including the condition of your home as well as how long it has been listed on the market. According to Zillow.com, the average home selling price in the US is $203,000 This

What are the key factors to consider when you invest in real estate?

You must first ensure you have enough funds to invest in property. You will need to borrow money from a bank if you don’t have enough cash. You also need to ensure you are not going into debt because you cannot afford to pay back what you owe if you default on the loan.

You must also be clear about how much you have to spend on your investment property each monthly. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

Finally, ensure the safety of your area before you buy an investment property. It would be a good idea to live somewhere else while looking for properties.

What is the maximum number of times I can refinance my mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. You can refinance in either of these cases once every five-year.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to become real estate broker

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

Next, pass a qualifying test that will assess your knowledge of the subject. This involves studying for at least 2 hours per day over a period of 3 months.

Once you have passed the initial exam, you will be ready for the final. For you to be eligible as a real-estate agent, you need to score at least 80 percent.

If you pass all these exams, then you are now qualified to start working as a real estate agent!