FHA loans are often used by first-time homebuyers because they offer more flexibility in terms of approval. FHA loans don't require any down payments and have credit scores below 620. This is in contrast to conventional loans which require 6%. You don't need to provide income verification or have your home appraised. FHA streamline also allows you to get an FHA loan even when you already own a home. However, the FHA streamline program does not allow you to refinance your old home into an FHA loan. This is unless you are investing in it. Moreover, the new mortgage cannot be an adjustable-rate mortgage (ARM) or a cash-out refinance.

Limits on multiple FHA loans

There are limitations on the number of FHA loans that a borrower may have at once. As a rule, borrowers are only allowed to obtain one FHA mortgage at a time, and they must pay off the first one before applying for another one. There are exceptions to this rule. It is possible for a borrower with certain circumstances to get two FHA loans.

Federal Housing Administration's (HUD) sets the limits for FHA loans. The number of units you have and the location of your property will affect the amount of money that you can borrow. For homes with multiple units, the limits are higher.

Minimum down payment

FHA loans are available only to those who have a down payment of at least 10% of the purchase cost. The government and state offer assistance programs for down payments if you don't have the funds. As part of your downpayment, you can also get a gift from family or friends. Make sure the gift is a gift, not a loan, as the FHA cannot approve a loan that involves borrowing to pay for the down payment.

You must also meet income and credit requirements. FHA loans require you to show proof of identity and assets. You must also have at least a 500 credit score to qualify. A low credit score will result in a higher interest rate. It is therefore important to be aware of your credit score.

To be eligible for an FHA loan, you must meet certain requirements

When you apply for an FHA loan, you need to prove that you can afford the monthly payments. To prove your income, you will need to provide proof such as bank statements, pay stubs and tax returns. Also, you should have enough financial reserves to pay the down payment and closing costs for a new house.

It is important to know the minimum amount of debt-to-income (DTI) when applying for loans. FHA requires that borrowers maintain a DTI below 43%. However, some lenders may accept applicants with higher DTI ratios. In determining your eligibility for loans, credit scores are also important.

There are some requirements to be eligible for an FHA loan.

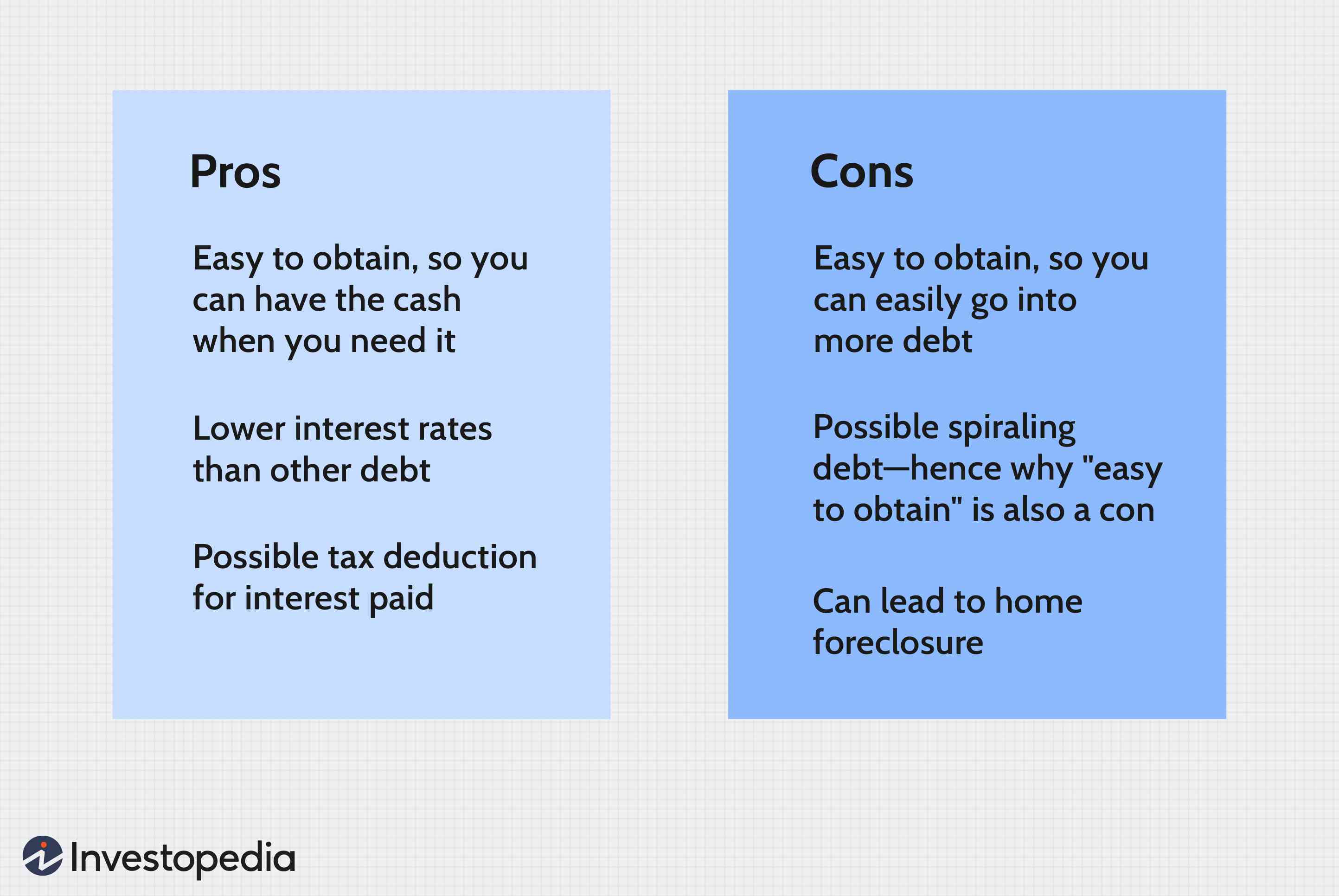

FHA loans are not easy to get a mortgage for people who have low credit ratings or don't have enough money down. FHA loans are usually cheaper than conventional mortgages because they are insured by government. Also, FHA lenders do not charge risk-based mortgage insurance. This means even those with bad credit have a greater chance of getting approved.

There are some questions you might have about your eligibility for a new loan if your home has been foreclosed. There are some requirements you need to fulfill in order to get an FHA loan after a foreclosure. You must have a minimum 20% income, credit reports that show positive changes and a 20% down payment. Be aware of the FHA loan eligibility rules, which will make it easier for your to get approved.

There are several ways you can qualify for an FHA Loan after the waiting period

After you have completed a waiting period, there are several ways that you can be eligible for an FHA Loan. One way is to prove that you have paid 12 months of mortgage payments and that your credit has improved since the beginning of your waiting period. FHA loans are only available to people with at least 580 credit scores. If you have had a foreclosure or any other credit-related event in the past, some lenders may require a higher score.

Some lenders will consider granting exceptions to borrowers with bankruptcy filings. You can file for bankruptcy due to financial hardships or an unplanned event like a medical emergency. People who file for bankruptcy can put a bad mark on their credit report. Many end up losing their homes because they have to file. However, if you can prove that you have recovered financially, you can qualify for an FHA loan after a bankruptcy.

FAQ

How long does it take to get a mortgage approved?

It all depends on your credit score, income level, and type of loan. It usually takes between 30 and 60 days to get approved for a mortgage.

Is it possible for a house to be sold quickly?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. There are some things to remember before you do this. First, you will need to find a buyer. Second, you will need to negotiate a deal. Second, prepare the house for sale. Third, your property must be advertised. You must also accept any offers that are made to you.

What is the maximum number of times I can refinance my mortgage?

This will depend on whether you are refinancing through another lender or a mortgage broker. In either case, you can usually refinance once every five years.

How long does it take to sell my home?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It can take anywhere from 7 to 90 days, depending on the factors.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

Finding an apartment is the first step when moving into a new city. This requires planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. There are many ways to do this, but some are easier than others. Before renting an apartment, you should consider the following steps.

-

Online and offline data are both required for researching neighborhoods. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Local newspapers, real estate agents and landlords are all offline sources.

-

Review the area where you would like to live. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also check out the local library and read articles in local newspapers.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what they liked and didn't like about the place. Ask them if they have any recommendations on good places to live.

-

Be aware of the rent rates in the areas where you are most interested. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out all you need to know about the apartment complex where you want to live. What size is it? How much is it worth? Is the facility pet-friendly? What amenities does it offer? Are there parking restrictions? Are there any special rules that apply to tenants?