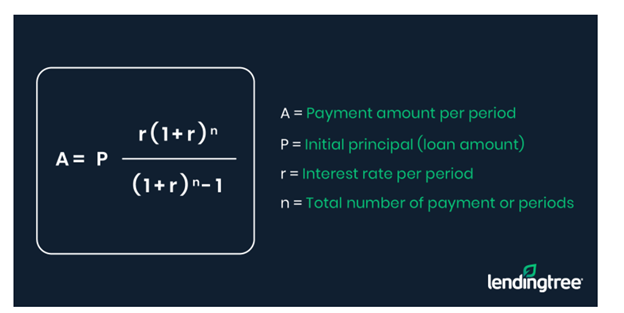

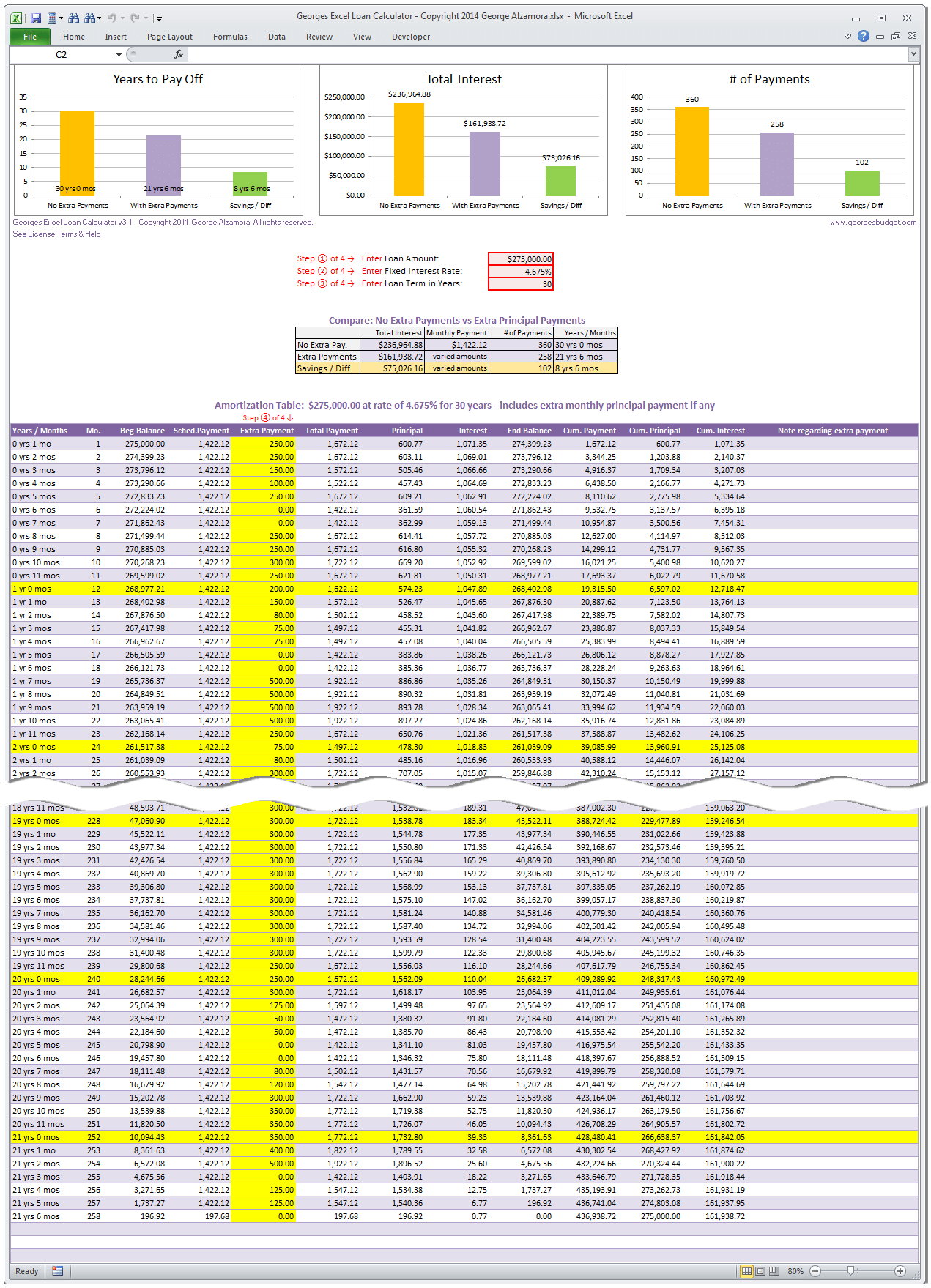

Interest-only mortgages have an adjustable rate and don't have fixed interest rates. These mortgages are not for everyone. They require some discipline but can be a great option for those with variable incomes. These mortgages are expensive. For an accurate understanding of your options, it is a good idea to consult an interest only mortgages calculator. The calculator will show how your repayment plan will change throughout the loan term. It will also tell you how much each month you should expect to be responsible for.

Adjustable-rate mortgages can be interest-only.

Interest-only mortgages are a common type of adjustable-rate mortgage (ARM). Unlike a traditional fixed-rate mortgage, interest-only mortgages can fluctuate based on the prime rate. The interest rate for an interest-only mortgage is typically lower than a fixed-rate mortgage, but borrowers must compare the interest rate and the length of interest-only periods before deciding which mortgage to get. Once the interest-only period ends, the monthly payment for an interest-only mortgage will rise, often substantially. A high monthly payment can lead to financial hardship.

Interest-only mortgages are not for everyone. If you're looking to buy a new home, it is important to first build equity, then refinance the loan in the future. However, it's important to keep in mind that an interest-only mortgage can lead to negative amortization, which means your mortgage balance could be higher than the value of your home. A qualified loan officer can help you to avoid this problem.

They require a lot discipline

For homebuyers who don't intend to live in their homes for long periods of time, interest only mortgages can be a great option. It's possible for you to get more square footage, but you don't have control over the housing market. You still owe the full mortgage amount even if your home's worth decreases. You must exercise discipline when paying this type of loan.

These mortgages can be used to finance high-end property and are very popular with investors. The principle isn't repaid until the property sells, which can be more than a decade after it was purchased. The interest-only loan is a great option if your ability to invest aggressively. Interest only loans typically have lower monthly payments than traditional mortgages. This option is only viable when the equity in the home exceeds the loan's value.

These can be very expensive.

Because of their low monthly payment, interest-only mortgages can be attractive to many. These mortgages come with risks, so borrowers need to be aware of them. Even though the monthly payments are lower, interest only mortgages can be more expensive over the life of the loan. This is because the lower monthly cost is not offset by the higher interest rate.

The borrower should consider the consequences of interest-only mortgages. If they have plans to sell the home in the future, they must be aware that they could face difficulties repaying the loan.

These can be a great option for those with variable incomes.

If you have variable income, interest only mortgages are a great option for you. Interest-only loans allow you to make lower monthly payments in times of low income. Just keep track the maturity date of your loan and make payments toward principal as soon as you can.

Interest-only mortgages have one drawback: you don't build equity in the home. This is especially true if your income is fluctuating or changes frequently. You can't refinance your home if it drops in value. While interest-only mortgages can be an option for people who have a variable income, it's important to remember that they can be risky.

FAQ

Should I rent or own a condo?

Renting is a great option if you are only planning to live in your condo for a short time. Renting allows you to avoid paying maintenance fees and other monthly charges. However, purchasing a condo grants you ownership rights to the unit. The space is yours to use as you please.

What should you look out for when investing in real-estate?

The first thing to do is ensure you have enough money to invest in real estate. If you don’t save enough money, you will have to borrow money at a bank. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

It is also important to know how much money you can afford each month for an investment property. This amount should include mortgage payments, taxes, insurance and maintenance costs.

You must also ensure that your investment property is secure. It would be a good idea to live somewhere else while looking for properties.

How can I fix my roof

Roofs can burst due to weather, age, wear and neglect. Roofers can assist with minor repairs or replacements. Contact us for more information.

How long will it take to sell my house

It depends on many factors including the condition and number of homes similar to yours that are currently for sale, the overall demand in your local area for homes, the housing market conditions, the local housing market, and others. It can take anywhere from 7 to 90 days, depending on the factors.

How much should I save before I buy a home?

It all depends on how many years you plan to remain there. It is important to start saving as soon as you can if you intend to stay there for more than five years. However, if you're planning on moving within two years, you don’t need to worry.

What should you look for in an agent who is a mortgage lender?

A mortgage broker is someone who helps people who are not eligible for traditional loans. They look through different lenders to find the best deal. This service may be charged by some brokers. Some brokers offer services for free.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. It can be difficult to find the right home. When choosing a house, there are many factors that will influence your decision making process. These factors include price, location, size, number, amenities, and so forth.

You can get the best deal by looking early for properties. Consider asking family, friends, landlords, agents and property managers for their recommendations. You'll be able to select from many options.