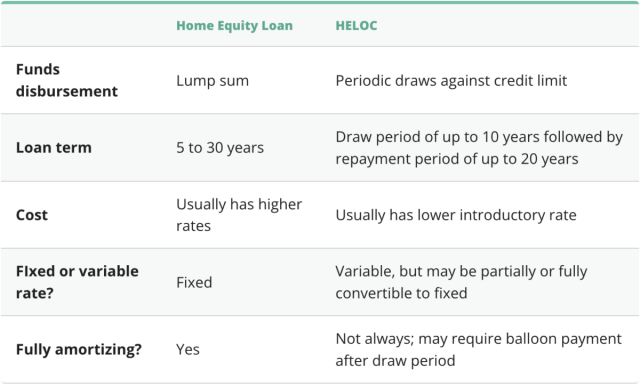

A home equity loans, also known by the HELOC, are a type of home equity credit. Its amount depends on several factors, including the equity in your home, your credit score, your loan-to-value ratio, and your debt-to-income ratio. You should not borrow more than 90% the value of your home.

Home equity loan

Consider your needs before deciding between a loan for home equity or a cash out refinance. A home equity loan could be a better option for several reasons. It may have a lower interest, lower closing costs and require no credit check. A cash out refinance, on the other hand, can be a better choice for certain uses such as consolidating debts or replacing your current mortgage loan.

Both options are available to homeowners. The biggest difference between a home equity loan and a refinance cash out is that a home equity line of credit (HELOC) does not change the terms of your primary mortgage. The home equity loan interest will be paid independent of your primary mortgage and will likely come with its terms and conditions. A HELOC interest may be tax-deductible. Home equity loans may also have additional costs such as closing costs and application fees.

Refinance using cash-out

A home equity mortgage is a great option to increase your cash flow without having to take out another mortgage. The loan can also be used to consolidate your debts, make large-ticket purchases, or improve your home. The process of cash-out refinances is usually easier if you have a low amount of debt to income ratio. So borrowers with poor credit should consider this option.

Cash-out refinances are typically longer-term and cost more than a home equity loan. A home equity mortgage may be a better option if your property has significant equity and you are looking to reduce the monthly mortgage payment. It is important to research all options thoroughly before making a final choice. A mortgage specialist is able to give you the information you need to make an informed choice.

A cash-out refinance differs from a home equity mortgage loan in that you must have mortgage insurance. A cash-out refinance usually requires mortgage insurance, which protects the lender in case you default on the loan. To be able to reach this level, you will need mortgage insurance. Once you have met this threshold, however, you can usually cancel the insurance.

Credit line for home equity

If you need extra cash, a home equity credit line may be an option. But you must be careful, as you may end up making larger monthly payments. Refinancing your property with a cashout refinance may change the terms and increase your debt. This can lead to financial difficulties, especially if you have had to reduce the property value since you obtained the loan.

If you need to borrow against the equity in your home to cover major expenses, such as college tuition, medical bills, or other high-interest debt, a home equity line of credit might be the best choice. Each option has advantages and disadvantages. You should weigh all of them carefully before you decide which one to choose.

If you have poor credit and need money quickly, home equity lines of credit loans may be an option. A minimum credit score requirement for home equity lines of credit is 580. In order to be eligible, you need to have a minimum equity of 15% in your home.

FAQ

Is it possible to sell a house fast?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. But there are some important things you need to know before selling your house. First, you will need to find a buyer. Second, you will need to negotiate a deal. Second, prepare the house for sale. Third, you need to advertise your property. Finally, you need to accept offers made to you.

What are the benefits associated with a fixed mortgage rate?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This means that you won't have to worry about rising rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

How can I find out if my house sells for a fair price?

Your home may not be priced correctly if your asking price is too low. A home that is priced well below its market value may not attract enough buyers. For more information on current market conditions, download our Home Value Report.

How long does it take to get a mortgage approved?

It depends on several factors including credit score, income and type of loan. It generally takes about 30 days to get your mortgage approved.

What is a Reverse Mortgage?

Reverse mortgages are a way to borrow funds from your home, without having any equity. It allows you access to your home equity and allow you to live there while drawing down money. There are two types: conventional and government-insured (FHA). If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. FHA insurance covers repayments.

What are the cons of a fixed-rate mortgage

Fixed-rate loans have higher initial fees than adjustable-rate ones. You may also lose a lot if your house is sold before the term ends.

What can I do to fix my roof?

Roofs can burst due to weather, age, wear and neglect. For minor repairs and replacements, roofing contractors are available. Contact us to find out more.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

When you move to a city, finding an apartment is the first thing that you should do. This process requires research and planning. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. This can be done in many ways, but some are more straightforward than others. These are the steps to follow before you rent an apartment.

-

Data can be collected offline or online for research into neighborhoods. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Local newspapers, real estate agents and landlords are all offline sources.

-

See reviews about the place you are interested in moving to. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. Local newspaper articles can be found in the library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what the best and worst things about the area. Ask for recommendations of good places to stay.

-

You should consider the rent costs in the area you are interested. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out information about the apartment block you would like to move into. For example, how big is it? What is the cost of it? Is it pet friendly What amenities do they offer? Are there parking restrictions? Are there any rules for tenants?